Can Europe Really Dump Its US Debt Holdings?

Michael Ross

Michael RossEU leaders considered weaponizing US debt amid geopolitical friction, but this 'nuclear option' faces significant ownership and market hurdles.

Recent geopolitical friction between the United States and the European Union, sparked by tensions over Greenland, has put a spotlight on the deep economic ties that bind them. As European leaders evaluate their strategic options against potential US pressure, one controversial idea has emerged: offloading their massive holdings of US debt.

While a "framework of a deal" reached at Davos has temporarily cooled the situation, EU nations are still preparing for future escalations. Two powerful countermeasures have been discussed. The first is a "trade bazooka" that would block US companies from the vast EU market, costing them billions. The second, more drastic option, involves selling off the trillions of dollars in US assets held across Europe.

But is this financial "nuclear option" actually feasible? Dumping such a large volume of assets could destabilize the global economy and create severe knock-on effects for the US financial system, including its exposure to the growing stablecoin market.

The 'Nuclear Option': Weaponizing US Debt

Before January 21, European officials openly explored their leverage. While Denmark deployed special forces to Greenland, other leaders focused on economic retaliation.

Former Dutch Defense Minister Dick Berlijn suggested that Europe could use its holdings of US debt as a powerful negotiating tool. "If Europe decides to offload those bonds, it creates a big problem in the US," he said. "[The dollar] crashes, high inflation. The US voter won't like that."

This view is shared by some financial analysts. George Saravelos, Deutsche Bank's chief FX strategist, highlighted America's core vulnerability in a recent note. "For all its military and economic strength, the US has one key weakness: it relies on others to pay its bills via large external deficits," he wrote.

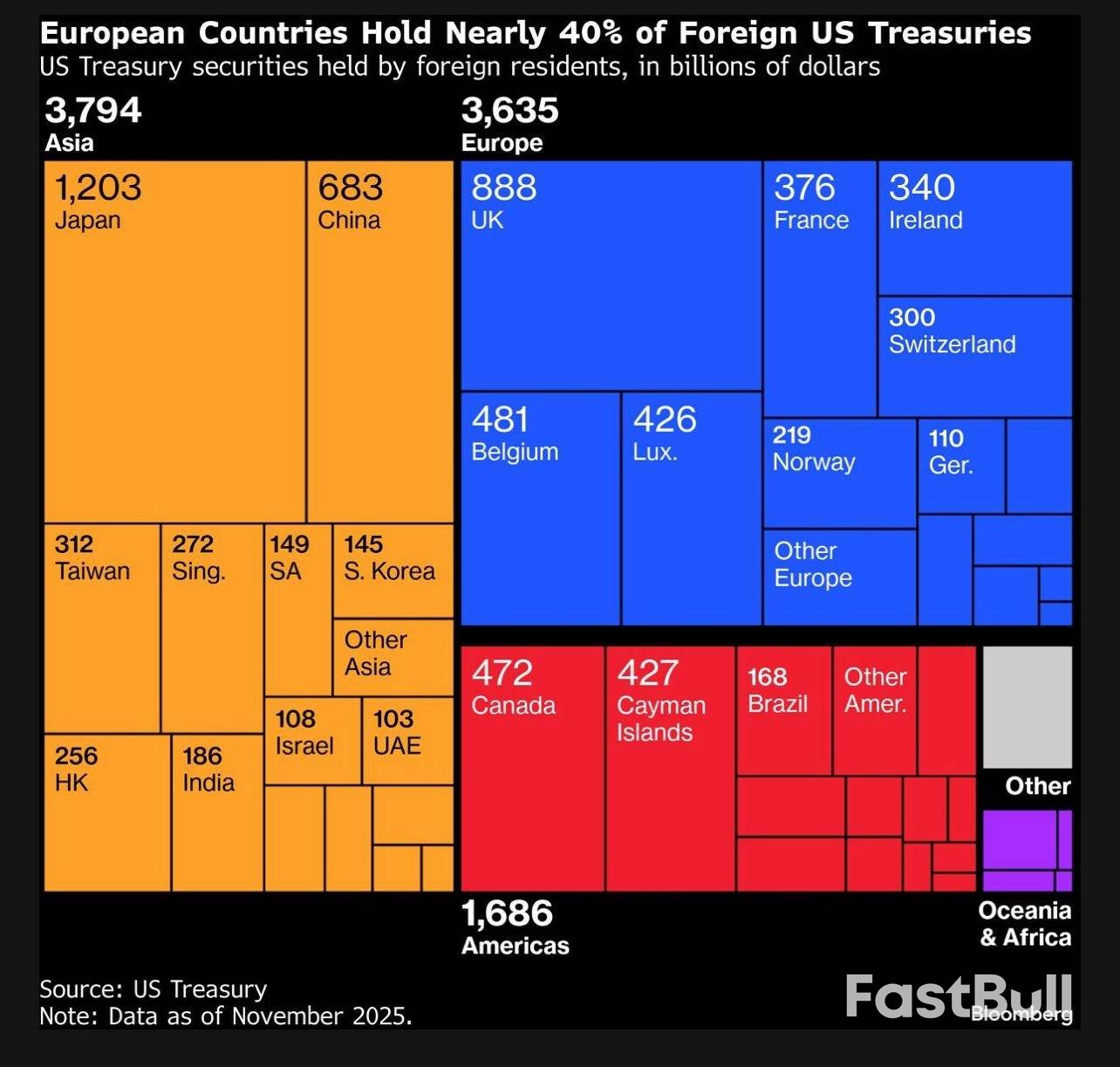

Figure 1: This chart breaks down foreign ownership of US Treasury securities as of November 2025. Europe holds a substantial $3.635 trillion, second only to Asia's $3.794 trillion, underscoring its significant financial leverage.

Saravelos pointed out that Europe holds $8 trillion in US bonds and equities, which he described as "twice as much as the rest of the world combined." The question is whether Europe can realistically liquidate these assets.

Major Hurdles to a Mass Sell-Off

Executing a coordinated sale of US debt faces significant practical challenges, from compelling private owners to sell to finding enough buyers in a de-dollarizing world.

The Ownership Puzzle: Public vs. Private

A key obstacle is that European governments don't directly own most of this debt. According to the Financial Times, the majority is held by private institutions like pension funds, banks, and corporate investors.

Yesha Yadav, a law professor and associate dean at Vanderbilt University, told Cointelegraph that "foreign government buyers tend to be sticky," meaning they are unlikely to sell unless absolutely necessary. Moreover, hedge funds in the UK, Luxembourg, and Belgium have become major purchasers of US Treasurys.

Forcing these private entities to sell for political reasons is a tall order. "It does not seem likely in the near term that European governments may impose restrictions on hedge funds buying US Treasurys," Yadav said. Kit Juckes, chief FX strategist at SocGen, added that the situation would need to "escalate a fair bit further before they damage their investment performance for political purposes."

The Scarcity of Alternatives

Even if Europe could orchestrate a sale, there is a fundamental problem: a lack of viable alternatives. US Treasurys are still considered the world's primary "risk-free" asset due to their unparalleled liquidity and stability.

"Even as other highly stable and safe countries, such as Germany, begin to issue debt, their debt markets remain relatively small, such that it is very difficult to envision them ever taking the place of the US Treasury market," explained Yadav.

Where Are the Buyers?

Finding buyers for trillions of dollars in US assets would be another immense challenge. China, once a primary buyer, has been steadily reducing its purchases of US debt.

Other Asian markets lack the capacity to absorb such a massive sell-off. The MSCI All-Country Asian index has a market capitalization of around $13.5 trillion, while the FTSE World Government Bond Index is about $7.3 trillion.

Analysts at Rabobank summarized the dilemma: "While the US's large current account deficit suggests that in theory there is the potential for the USD to drop... the sheer size of US capital markets suggests that such an exit may not be feasible given the limitations of alternative markets."

The Stablecoin Factor: A New Force in the Treasury Market

As traditional foreign buyers reconsider their positions, a new and powerful player has entered the market for US debt: stablecoin issuers.

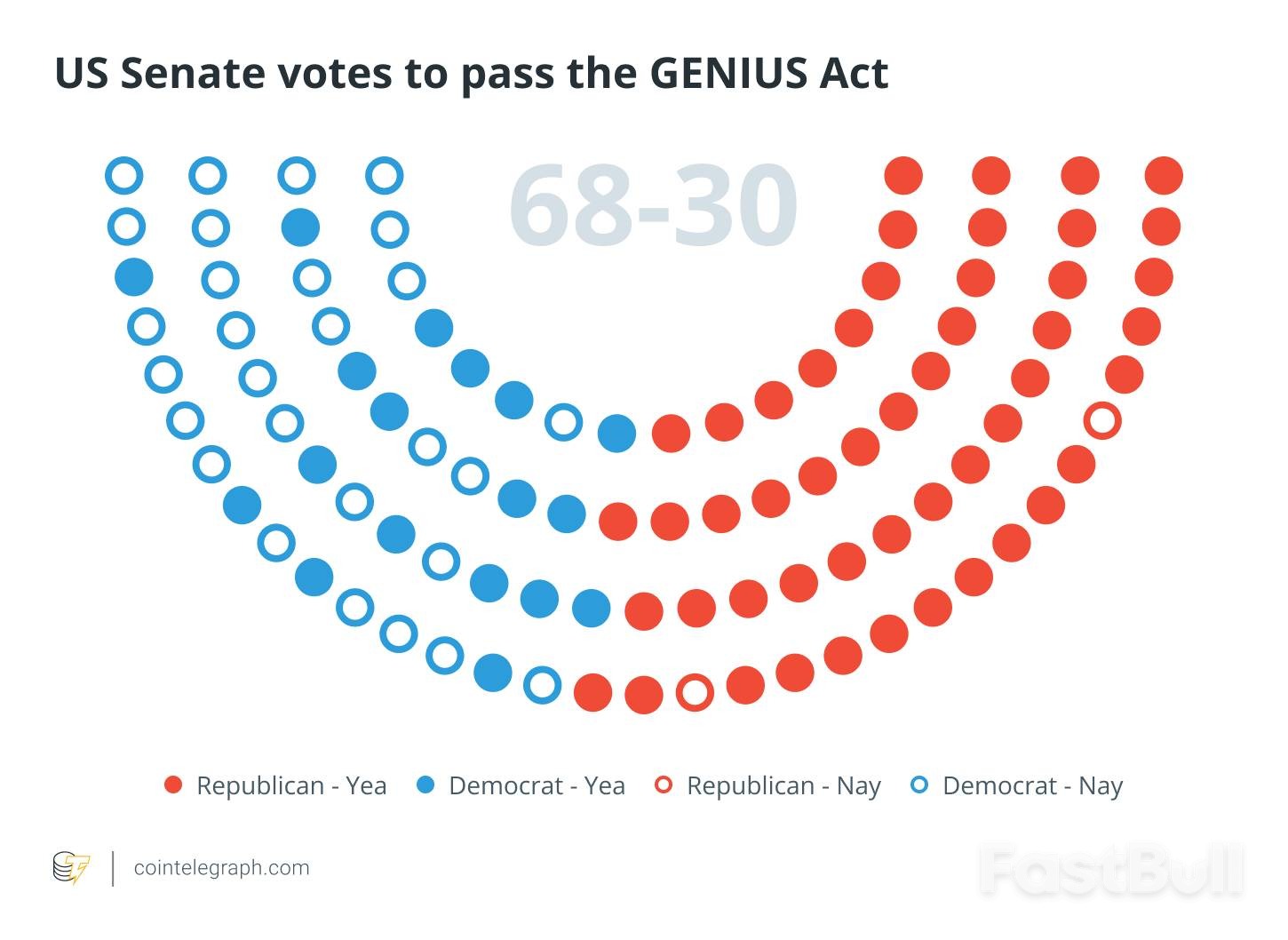

Figure 2: The US Senate's passage of the GENIUS Act established a regulatory framework requiring stablecoin issuers to back their assets with dollars and US Treasurys, creating a new, structural source of demand for government debt.

Landmark US legislation known as the GENIUS Act mandates that stablecoin issuers operating in the country must hold reserves in dollars and US Treasurys to back their coins. This has created a significant new source of demand for government bonds.

"That [stablecoin issuers] are growing as fast as they are means that their need for Treasurys is correspondingly high," said Yadav. "To the extent that this trend continues, it offers a great advantage for US policymakers."

However, this growing dependency also introduces new risks. It deepens the link between the stability of the crypto market and the liquidity of the US Treasury market.

This reliance could become a critical vulnerability, especially if a major holder like the EU were to reduce its exposure. Yadav and Brendan Malone, formerly of the Federal Reserve Board, have highlighted past liquidity shocks in US debt markets in March 2020 and April 2025. A sudden run on stablecoins could force issuers to rapidly sell their Treasury holdings. In a market with fewer traditional buyers, this could trigger a liquidity crisis, damage the credibility of US debt, and potentially render an issuer insolvent.

An Uncertain Future for Alliances and Markets

The strategic rivalry in an increasingly multi-polar world is creating fractures between historic allies. While dialogue between the EU and US continues, the underlying tensions remain.

"We are not yet out of the woods," warned Latvian President Edgars Rinkēvičs. "Are we in an irreversible rift? No. But there is a clear and present danger." That danger threatens not only the sovereignty of nations like Greenland but also the stability of the US debt markets that underpin the global financial system.