BoE's Shock 5-4 Vote Puts GBP on Notice

Kevin Morgan

Kevin MorganA close 5-4 BoE vote for a rate hold signals future cuts despite strong PMI data and dovish forecasts.

The Bank of England (BoE) has held its key interest rate steady at 3.75%, but a surprisingly close 5-4 vote has signaled a dovish shift, increasing the likelihood of future rate cuts.

While the decision to maintain the Bank Rate was expected, the narrow margin suggests the Monetary Policy Committee (MPC) is more divided than anticipated. This development has raised market expectations for a rate cut as early as March, though the final outcome will depend heavily on two upcoming labor market reports and inflation prints.

A Surprisingly Divided Monetary Policy Committee

Four members of the committee dissented from the decision, voting instead to lower rates. The dissenters were Dhingra, Taylor, Ramsden, and Breeden.

The votes from Ramsden and Breeden were particularly noteworthy, as recent economic data had, if anything, pointed toward a more hawkish stance since the December meeting. Both members cited new analysis in the latest monetary policy report as a key factor in their decision, highlighting that structural changes in wage-setting are no longer expected to add significant inflationary pressure.

BoE Forecasts Weaker Growth and Slower Inflation

The Bank of England's new monetary policy report paints a distinctly more dovish picture of the UK economy. Compared to its November projections, the BoE now anticipates lower GDP growth, higher unemployment, and softer inflation.

Key forecast revisions include:

• CPI Inflation: Now projected to be 1.7% in the first quarter of 2027, down from the previous forecast of 2.2%.

• Annual GDP Growth: Revised downward by 0.3 percentage points to 1.2%.

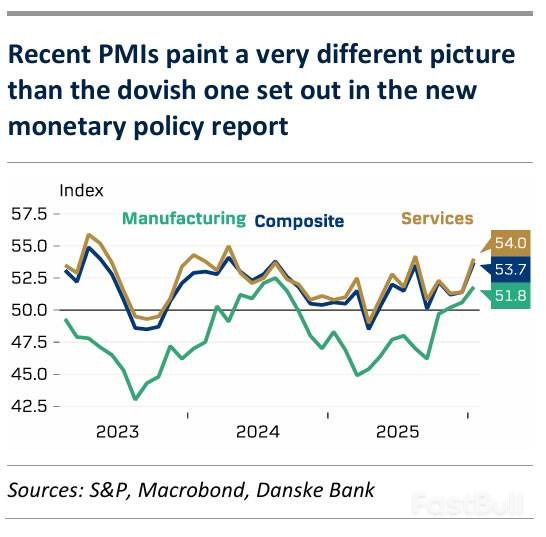

Contrasting Signals from Recent Economic Data

This cautious outlook from the BoE contrasts sharply with recent PMI data, which suggests a more robust economy. The composite PMI recently hit its highest level in three years, and price indices within the report indicate that inflationary pressures could be more sustained. Upcoming data will be crucial in clarifying which of these conflicting signals more accurately reflects the state of the UK economy.

Figure 1: Recent UK PMI data shows a strengthening economy, with the composite index at a three-year high, contrasting with the Bank of England's more cautious economic forecast.

Outlook for UK Rates and the British Pound

The timing of the next rate cut appears to rest heavily on Governor Andrew Bailey, who has indicated a readiness to ease policy. Bailey noted that the two cuts currently priced in by markets seem fair.

While the timing will ultimately hinge on incoming data, the bar for further cuts has likely been raised as the Bank Rate approaches neutral levels. A first rate cut is projected for April, with another potentially following in November.

In currency markets, the EUR/GBP pair traded higher following the announcement, supporting expectations for a weaker pound. The forecast for EUR/GBP is 0.89 over a 12-month horizon, driven by narrowing interest rate differentials, a relatively weaker growth outlook for the UK, and a positive correlation to a weaker U.S. dollar environment.